%20(1)%202.svg)

Asset-Based Lending vs. Traditional Bank Loans: What Growing CPG Brands Need to Know

If you’re running a growing consumer brand, chances are you’ve run into this familiar gap: your products are selling, demand is strong, but the capital to fund inventory, marketing, and growth in general just isn’t moving at the pace you need. Whether it is extended payment terms from retailers or the upfront cost of scaling DTC, the cash conversion cycle can quickly become a constraint on growth. Most brands start by approaching their bank, but after a lengthy underwriting process, they find a structure built around stability, not scale. Personal guarantees, restrictive covenants, limited availability against inventory, and long approval times are common. These terms work well for established businesses with steady cash flows and minimal seasonality, but they’re not built for high-growth CPG brands operating across DTC, Amazon, retail, and wholesale.

That is where asset-based lending comes in. ABL offers a more flexible path to working capital, based on\ the value of your receivables and inventory, not just your balance sheet. It’s not a one-size-fits-all solution, and it is not right for every business. But for the brands it is built for, it can be transformative.

Why Traditional Bank Financing Often Falls Short for Modern CPG Brands

Traditional banks aren’t in the business of rapid growth—they’re in the business of risk mitigation. Their products are designed to serve a broader base of companies, many of which have steady cash flow and a long track record of profitability. That’s the challenge for emerging brands with fast-moving business models and omnichannel distribution strategies.

1. Long and Rigid Approval Processes

Banks typically require extensive historical financials, tax returns, audited statements, and months of documentation before issuing a decision. For early-stage CPG businesses, the process can feel misaligned with the speed at which their operations move. Even once approved, drawing down capital can be slow and tied to tight controls.

2. Strict Covenants and Personal Guarantees

To manage risk, banks often require businesses to maintain specific financial ratios (like debt-to-equity or interest coverage) or impose restrictions on how capital can be used. Many also require personal guarantees from founders—a non-starter for those looking to build their companies without putting personal assets on the line.

3. Limited Flexibility Against Inventory or POs

Most traditional lenders are hesitant to provide credit against inventory, especially if it's perishable or seasonal. Purchase order financing? Rarely offered. This creates a disconnect between how capital is issued and how a brand’s expenses actually occur.

4. Lockbox and Cash Dominion Requirements

Many banks require lockbox accounts or full cash dominion, meaning the lender controls incoming revenue and applies it directly to the loan. For consumer brands managing cash flow across multiple channels and vendors, this can create friction and slow down operations.

What Is Asset-Based Lending?

Asset-based lending is a form of secured financing where a business borrows against its assets, typically accounts receivable and inventory. In contrast to traditional loans that focus on credit history or cash flow ratios, ABL is primarily concerned with the quality and value of the collateral.

Here’s how it typically works:

- You receive a revolving line of credit.

- Your borrowing capacity is based on a percentage of eligible receivables (e.g., 90%) and inventory (e.g., 70%).

- As your sales and inventory grow, your available credit line increases.

- Repayment is often tied to incoming payments on receivables, but without restrictive lockbox arrangements.

Why ABL Fits the Needs of High-Growth CPG Brands

For brands in high-demand consumer categories like food & beverage, beauty, health & wellness, apparel, and home goods, asset-based lending is often a better fit—because it’s built for businesses that move fast, reinvest constantly, and have valuable working capital tied up in product and receivables.

1. Access to Capital That Grows With You

With ABL, your available credit isn’t capped arbitrarily—it expands with your inventory and receivables. This makes it ideal for brands entering new retail accounts, scaling DTC, or managing seasonal demand.

2. Fewer Restrictions and Greater Flexibility

Most ABL lenders don’t require personal guarantees, lockboxes, or burdensome covenants. You retain more control over how and when capital is used. That flexibility can make a critical difference in how quickly and confidently you’re able to move.

3. Receivables and Inventory Treated as Assets, Not Liabilities

Instead of viewing inventory as a cost center, ABL recognizes it as an asset. This can unlock significantly more capital than a traditional working capital loan, especially when paired with receivables from established retail partners or major DTC volume.

4. Faster Time to Close and Fund

ABL lenders understand the growth trajectories and business models of consumer brands. Underwriting is typically faster and more focused on what actually matters—your customers, your products, and your assets.

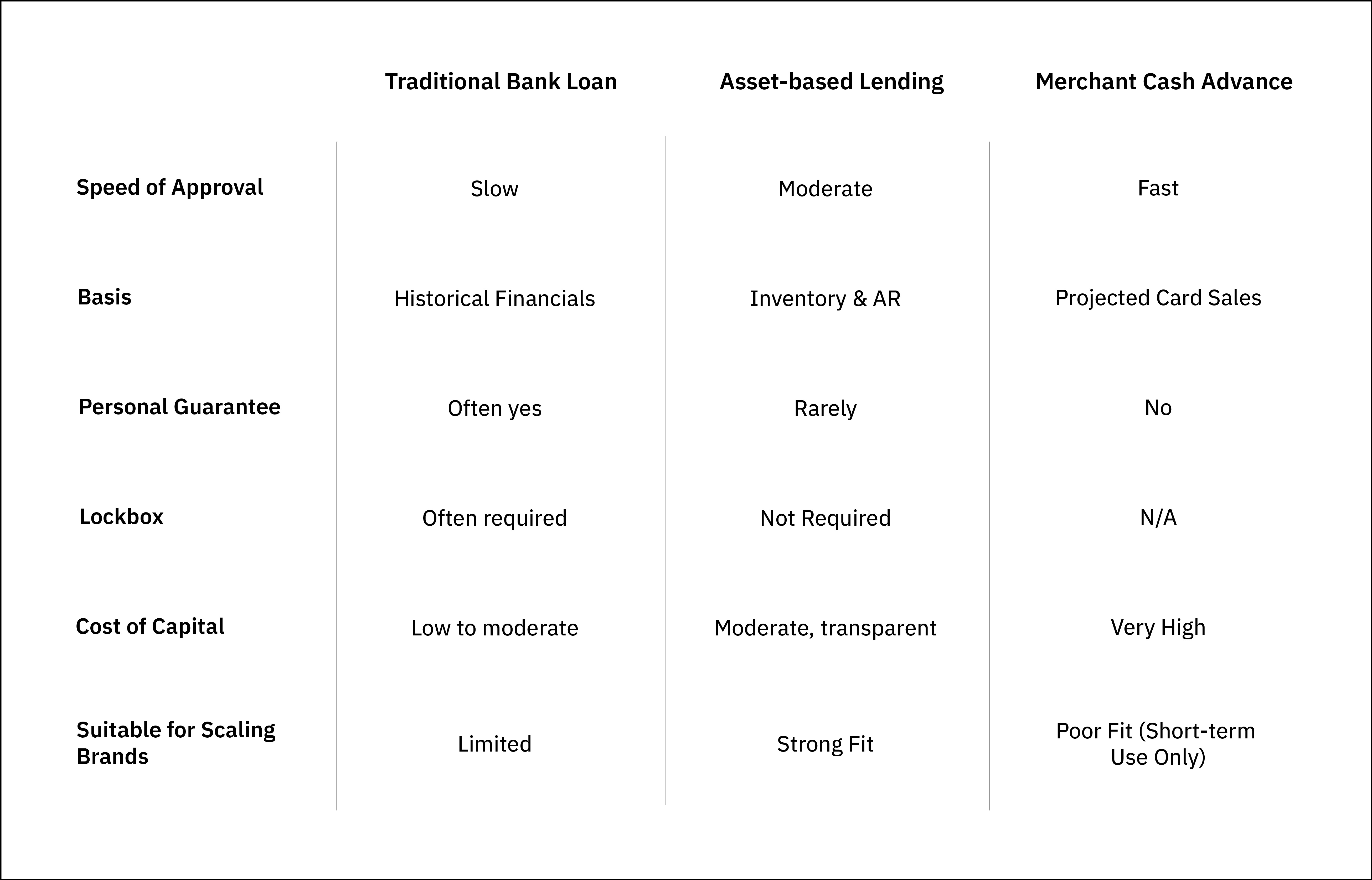

Comparing the Options: Bank Loans vs. ABL vs. Merchant Cash Advances

Let’s break it down with a practical comparison:

When ABL Makes the Most Sense

Asset-based lending isn’t right for every business, but it’s a strong option for brands that:

- Have $5M+ in revenue and are looking to scale.

- Sell across multiple channels (DTC, Amazon, retail, wholesale).

- Have reliable retail receivables or strong DTC sales.

- Carry meaningful inventory or need upfront capital for production.

- Are venture-backed or profitable but need working capital without dilution.

If your biggest obstacle is the timing of cash, in other words, you know how to grow, you just need the resources to do it—ABL can bridge that gap.

A Real-World Scenario: Using ABL to Fund Expansion

Consider a $10M clean skincare brand preparing to expand into national retail while maintaining strong DTC and Amazon channels. Retailers require 60-day terms. Inventory needs to be paid for now. The brand has already proven sell-through and is confident in the next stage, but capital is tight.

A bank might offer a $750K line of credit tied to prior years’ profitability and require a personal guarantee. An MCA could deliver cash fast, but at a 40%+ effective APR.

An asset-based lender, on the other hand, could provide a $2M revolving line based on existing receivables and inventory, with no personal guarantee and no restrictive covenants. That means the brand can invest in production, pay suppliers, launch into new stores, and continue fueling growth—all while maintaining ownership and control.

Choosing the Right Lending Partner

Choosing the right financing isn’t just about cost—it’s about structure, flexibility, and alignment with your growth plan. A good asset-based lender will:

- Understand how consumer brands grow and scale

- Offer terms that reflect your specific working capital needs

- Be transparent about pricing and structure

- Act as a true financial partner, not just a lender

How Assembled Brands Supports Scaling CPG Businesses

At Assembled Brands, we specialize in asset-based credit lines tailored to the needs of modern consumer businesses. Our structure is designed to be founder-friendly and growth-aligned.

Here’s how we support our partners:

- Credit lines up to $25M based on receivables and inventory

- Advance rates up to 90% on A/R and 70% on inventory

- No personal guarantees, no lockbox, no hidden fees

- The option to layer in PO financing

- Fast, transparent underwriting from a team that knows CPG

Whether you’re preparing for a new retail launch, ramping up marketing, or simply need more working capital to support demand, our goal is to provide financing that fits your model, not force you to fit ours.

Final Thoughts

Asset-based lending isn’t just an alternative to traditional bank financing—it’s a strategic tool for brands that are growing quickly and need capital to match their pace. For consumer businesses with meaningful receivables, strong inventory, and clear opportunities for scale, ABL can provide the flexibility and control that more conventional options lack.

If your brand is facing long cash conversion cycles, gearing up for expansion, or simply looking for a more aligned financing partner, it may be time to explore what asset-based lending can do for you.

At Assembled Brands, we work with today's top emerging CPG businesses—bringing deep category expertise and a financing structure built to support your growth, not slow it down.

Apply today to get started with a short online application, or reach out to our team to learn more. We’re here to help you find the right capital solution for where you’re headed next.

Related Articles

.avif)